On-Chain FI Assets: Tokenized Deposits & Instruments

Sample sequence of customers wanting to tokenize their own assets/coins- example bank deposits.

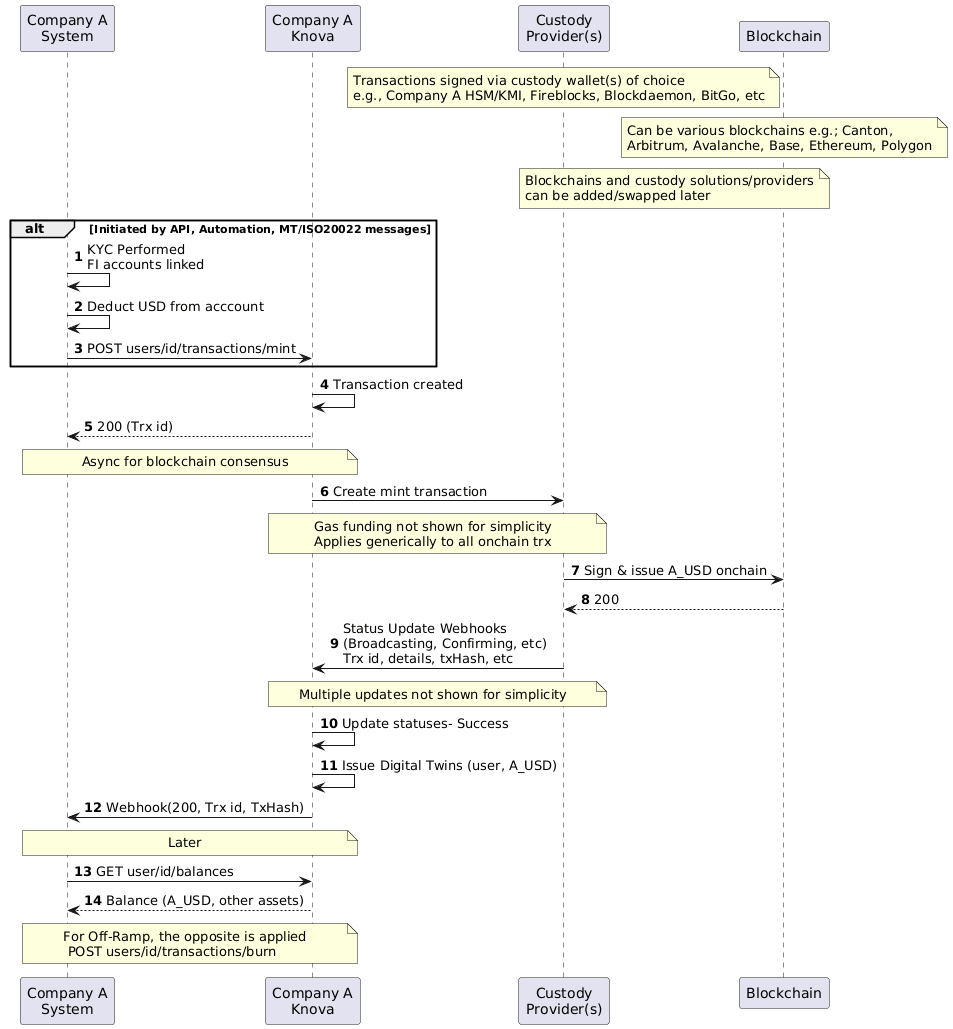

Suppose Company A is a financial institution that wants bring their assets, financial instruments, liabilities/obligations on-chain. This example uses tokenized deposits- A_USD, which is Company A's USD deposits issued on-chain to reap the benefits of tokenization.

Let's assume Company A has gone thorough the onboarding flow Onboarding & Asset Transfers, and has selected its desired blockchain and custody provider(s). Now they are ready to issue their assets on-chain.

Note- Knova keeps the solution blockchain and custodian-agnostic and can add/swap later with minimal impact to Company A.

- Company A issues tokenized representation of its cash deposits- A_USD (Steps 1-12)

- Any blockchains and custody providers can be used and swapped with minimal impact to Company A.

KYC and identity solutions of choice (e.g. Existing repos, W3C DID/VC) can be supported. - The entire process or subsets of the process can be initiated by Knova with automations or messages processors (e.g., MT/ISO 20022) connected to Company A systems, or by Company A through APIs. This allows for Company A to not change anything to do their existing systems and workflows, or augment with APIs where they see it within their system. Note this is possible as Knova is running within Company A's environment and firewalls.

- Knova handles all the interactions with Company A systems, smart contracts to issue A_USD, custodians to sign transactions, and selected blockchains. Knova creates Digital Twin representations to match onchain A_USD, and asynchronous blockchain updates are handled by Knova and real-time updates & notifications can be set with Company A systems.

- Any blockchains and custody providers can be used and swapped with minimal impact to Company A.

- Deposits/assets issued to User + confirming balances (Steps 13-14)

- A_USD is issued onchain and its Digital Twins are made available for Company A to transact and enable further tokenization use cases. These assets are made available for off-chain and on-chain transfers as explained in Onboarding & Asset Transfers.

- Note for any transactions, existing Company A flows can be incorporated, e.g. Account validation, compliance checks, data collection, alerts via email/SMS, notifications.

- Note behaviours can be different depending on asset type. In a indirect/omnibus model, assets are swept to Omnibus (e.g. A_USD may not need to reside in individual end users addresses and be swept to customer omnibus for simpler maintenance/audit/security/gas, while MMFs do not get swept and must reside with the end users)

Sample sequence of tokenization of Company A assets via blockchain and custody of choice

Additional Context on Tokenizing Financial Instruments

Automate and Streamline internal Bank Systems through Digital Assets

Knova was founded upon the principle of simplifying finance. Commercial banks face the dual challenge of managing complex traditional financial systems while preparing for the inevitable shift toward digital assets. Knova empowers banks with the tools to issue their own tokenized deposits, combining the stability of traditional banking with the flexibility of digital finance.

Current Problem and Future Opportunity

Commercial banks manage large-scale operations involving multiple asset classes across various systems, leading to inefficiencies in netting, settlement, reconciliation, and risk management. As the financial ecosystem evolves, banks are looking to adopt solutions that align with the rise of digital assets while maintaining regulatory compliance and operational efficiency.

Knova enables banks to tokenize their deposits, creating a unified and programmable solution for managing financial transactions. Tokenized deposits not only simplify internal processes but also provide a bridge to future-proof systems that are interoperable with digital asset networks.

Tokenized Commercial Bank Deposit Features

Knova’s tokenized deposit solution addresses challenges in reconciliation, settlement risk, fraud, lack of interoperability, and real-time monitoring between backend systems. By leveraging Knova’s tokenization ledger, commercial banks can achieve:

- Real-time transparency and control: Banks can view and manage tokenized deposits alongside traditional assets with real-time aggregate cash and asset monitoring.

- Programmable logic for deposits: Integrate regulatory and business logic directly into tokenized deposits (e.g., reserve requirements, automatic settlement rules).

- Streamlined reconciliation: Tokenized deposits allow seamless integration into a unified ledger, reducing the complexity of netting and settlement.

- Cost savings: Utilize off-chain and on-chain mechanisms to lower the operational costs of transaction management.

- Interoperability: Enable interactions between tokenized deposits and external blockchain ecosystems for future-ready operations.

Outcomes from Tokenized Deposits

The Knova Tokenized Commercial Bank Deposit solution enables:

- Improved efficiency: Reduce operational costs and complexities by managing tokenized and traditional deposits through a unified platform.

- Enhanced transparency: Real-time visibility into all tokenized and traditional assets under management.

- Regulatory compliance: Built-in tools to meet reserve and reporting requirements.

- Future-proof operations: Position banks to interact with digital asset networks and evolving payment infrastructures seamlessly.

- Strengthened trust and confidence: Customers and regulators benefit from enhanced transparency and streamlined operations.

Updated 7 months ago